Merchant Guide to Chargeback & Dispute Management

This guide helps you understand, navigate, and successfully defend against payment disputes (chargebacks). By following these standards, you can minimize revenue loss, maintain healthy processing history, and ensure strict compliance with Visa and Mastercard card scheme rules.

What is a Dispute and Its Nature?

Definition of Dispute

A dispute (commonly referred to as a chargeback) occurs when a cardholder contacts their card-issuing bank to challenge a transaction on their statement. When this happens, the funds are temporarily withdrawn from your merchant account and held by the card network until a final decision is made based on the evidence presented.

Categories of Disputes

Disputes are classified into specific scheme categories. Understanding why a transaction was disputed is the first step toward resolving or defending it:

| Nature | What is it | Scheme References |

|---|---|---|

| Fraud / Unauthorized Transaction | The cardholder claims they did not authorize or make the transaction, or that their card details were stolen and used in a Card-Not-Present (CNP) environment. | Visa Reason Code 10.4 (Other Fraud - Card-Absent) Mastercard Reason Code 4837 (No Cardholder Authorization). |

| Merchandise / Service Not Received or Delivered | The cardholder acknowledges authorizing the charge but asserts that the physical goods were never delivered or the digital/SaaS services were not rendered. | Visa Reason Code 13.1 Mastercard Reason Code 4855. |

| Not as Described or Defective | The cardholder received the items or accessed the services, but claims they were damaged, defective, completely different from the website description, or that a software service failed to live up to promised technical specifications. | Visa Reason Code 13.3 Mastercard Reason Code 4853. |

| Cancelled Recurring / Subscription Disputes | The customer claims that they cancelled their subscription or recurring billing agreement before the charge occurred, but your system charged them regardless. | Visa Reason Code 13.5 Mastercard Reason Code 4853. |

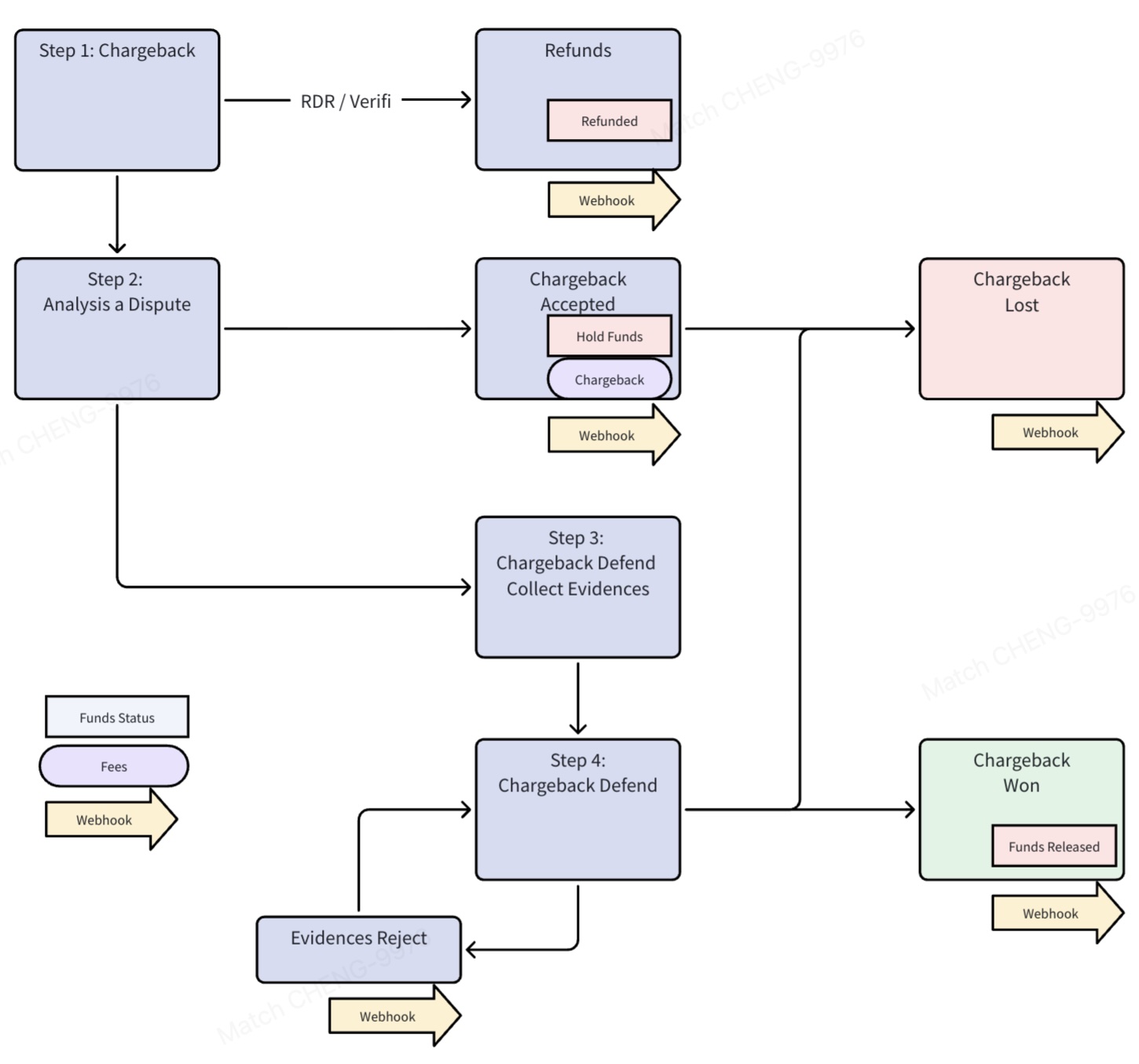

Chargeback Overall Flow

Notification of Disputes

At Evonet, Disputes are being notified in two major mechanisms:

- Webhook Notification from our Dispute API.

- Email Notification to your assigned destinations.

What to Do when a Dispute is Received

When a new dispute is logged against your account, time is your most critical constraint. You must follow this step-by-step operational workflow:

Step 1: Check the Deadline - Typically 10 days

Every dispute comes with a specific "Respond By" date determined by the card networks. Missing this deadline results in an automatic, irreversible loss of the dispute and the associated funds. Ensure your operational queue prioritizes files based on chronological expiry.

Step 2: Analyze the Validity of the Dispute

- Accept the Dispute: If you realize an error occurred (e.g., a subscription wasn't cancelled in time, or shipment tracking reveals a package was permanently lost), accept the dispute. Acceptances stop further scheme fees from escalating and prevent the case from moving to costly arbitration.

- Fight / Defend the Dispute (Representment): If your internal system logs, tracking numbers, or contracts demonstrate that the transaction was legitimate, completely authorized, and fully fulfilled, prepare to submit a structured evidence package.

Step 3: Compelling Evidence Requirements

To overturn a chargeback during the representment phase, the card network issuers require objective, verifiable data. Ensure your evidence document packages contain the specific parameters detailed below according to the nature of the dispute.

| Dispute Category | Primary Goal of Evidence | Key Documents to Compel & Upload |

|---|---|---|

| Fraud & Unauthorized Charges (10.4 / 4837) | Prove identity match or network-level liability shift | • 3DS Payload tokens (CAVV/UCAF) . • Visa CE3.0 Footprint: Provide 2 matching historical charges (120–365 days old) with identical IP/Device ID context . • Account validation records & login emails. |

| Services Not Received (13.1 / 4855) | Prove fulfillment of service or delivery of digital access | • A formal tracking receipt from a recognized logistics carrier (e.g., DHL, FedEx, UPS) showing the package status as successfully delivered. • Internal application/software server/ IP access logs displaying precise usage metrics, timestamps, and active user traffic. |

| Not as Described / Defective (13.3 / 4853) | Prove fulfillment perfectly matches contractual specification | • Screenshots, marketing materials, or cached product pages detailing exactly what was promised to the user at the moment of purchase. • Proof that the customer failed to return the physical goods or did not follow the explicit dispute mitigation processes outlined in your Terms of Service before initiating the bank dispute. |

| Canceled Subscription / Recurring (13.5 / 4853) | Prove explicit consent and absence of a valid, timely cancellation request | • A copy of the digital contract, checkout screen authorization checkbox, or signed agreement demonstrating that the customer opted into an ongoing recurring billing schedule. • Proof that your cancellation methods and timelines were prominently displayed during registration and remain accessible within the user portal. • A platform account log indicating that the user's cancellation request was submitted after the disputed renewal event, or that they continued to use premium platform tools after their alleged cancellation date. • Timestamps and email delivery receipts proving that a renewal warning notification was successfully sent to the cardholder's registered email address prior to executing the charge. |

Step 4: Fighting / Defend the Dispute

With the evidences collected, submit these evidences via our Web Portal or Dispute API.

Evonet will review the evidences submitted and then submit it to the card networks.

Step 5: Result notification - 60 days

After you submit your evidence package, the issuing bank has up to 45 to 60 days to review your defense documentation and issue a final verdict (either overturning the chargeback in your favor or sustaining it).

Proactive Tips for Reducing Disputes

The most profitable way to manage disputes is to prevent them from occurring in the first place:

Adapt 3D Secure or Apple Pay

3DS and Apple Pay comes with Liability Shift. Liability rules fundamentally dictate who bears the financial burden of a fraud-related chargeback.

- 3D Secure: If a transaction passes through EMV 3-DS and receives a ECI 05,06,01,02, a Liability Shift occurs. The financial liability moves from the merchant to the card issuer. In addition, most of these chargeback will be automatically defended or rejected at the network level.

- Under both Visa and Mastercard rules, a successfully tokenized Apple Pay transaction carries inherent network-level liability shift similar to a fully authenticated 3DS transaction. The issuer validates the token and cryptogram during authorization, passing liability downstream to themselves for fraud disputes.

By shifting liability to the card issuer, the merchant avoids funding the chargeback reversal out-of-pocket for legitimate fraud occurrences (Visa 10.4 / Mastercard 4837).

Billing Descriptor is Instantly Recognizable

If a customer looks at their online bank statement and does not recognize your merchant name, their immediate knee-jerk reaction is to tap "Report Fraud" in their banking app.

- What to do: Our Billing Descriptor is usually set to the brand name of your URLs, either the URL or the Brand name. Spelling must be correct. Use of Entity name is not preferred if it is not well known by the customer.

Clear descriptors eliminate accidental billing confusion, helping customers recognize their purchase instantly and bypassing the bank's customer service department entirely.

Adapt RDR / Ethoca

Do not wait for a formal chargeback letter to arrive in your dashboard. By that time, network damage is already done. Instead, use real-time alert networks to intercept angry or confused customers at the bank level.

- What to do: Contact your RM to activate Verifi RDR (Rapid Dispute Resolutions) and Ethoca that will cover both Visa and Mastercard transactions.

- How it works: When a customer calls their bank to claim an unrecognized charge, these networks pause the dispute and immediately notify your system. You can issue an automated instant refund to the customer right then and there.

Send Transparent "Pre-Billing" Renewal Warnings

Surprise subscription charges are the number one cause of "Friendly Fraud" (where customers call their bank simply because they forgot they signed up for an annual plan).

- What to do: For annual, high-ticket monthly, or post-trial recurring billing cycles, configure your system to send an automated, explicit email warning 3 to 7 days before charging their card.

- Make it bulletproof: * Use a clear subject line like: “Your subscription renews in 3 days.”

- State the exact amount and the card token that will be billed.

- Crucial: Include a prominent, single-click "Cancel Subscription" button directly inside the email.

Updated 2 months ago